FCA PS25/20 – Live from 6 April 2026

CCI compliance for investment managers. Automated.

The Consumer Composite Investments regime replaces UCITS KIID and PRIIPs KID with a single, flexible disclosure framework. Kurtosys automates every step – from calculating the Risk and Return Score to publishing compliant Product Summaries at scale.

6 Apr 2026

Optional CCI transition open now

8 Jun 2027

Mandatory deadline – firm, no extension

1 framework

UCITS KIID and PRIIPs KID

Trusted by

What is CCI

The UK's new retail disclosure framework

The Consumer Composite Investments (CCI) regime replaces both the PRIIPs Key Information Document and the UCITS Key Investor Information Document with a single, flexible Product Summary Document – finalised by the FCA in December 2025 under Policy Statement PS25/20.

The FCA’s own technical specialists described the old KID format as “dense, technical, and highly templated” – not widely read and not widely understood. CCI replaces prescribed templates with a principles-based framework.

Under PRIIPs, compliance was procedural. Under CCI, it’s interpretative – investment managers must exercise judgement at every step.

The FCA’s four Product Summary requirements

Technology neutral

Must work digitally and in print – no prescribed delivery medium.

Must genuinely help investors understand the product, not just satisfy a checklist.

Common metrics are standardised. Format and structure are at the firm’s discretion.

Investors must access the most relevant information easily, when they need it.

KEY DATES

Where we are - and what's coming

Legislation enacted

Final FCA rules published

Final KIID refresh

Live now

Optional transition

Full CCI mandatory

What the FCA requires

Six obligations every CCI manufacturer and distributor must meet

Under PRIIPs, compliance was procedural – follow the template, satisfy the checklist. Under CCI, it is interpretative. The six obligations below define what that means in practice.

01

Product summary document

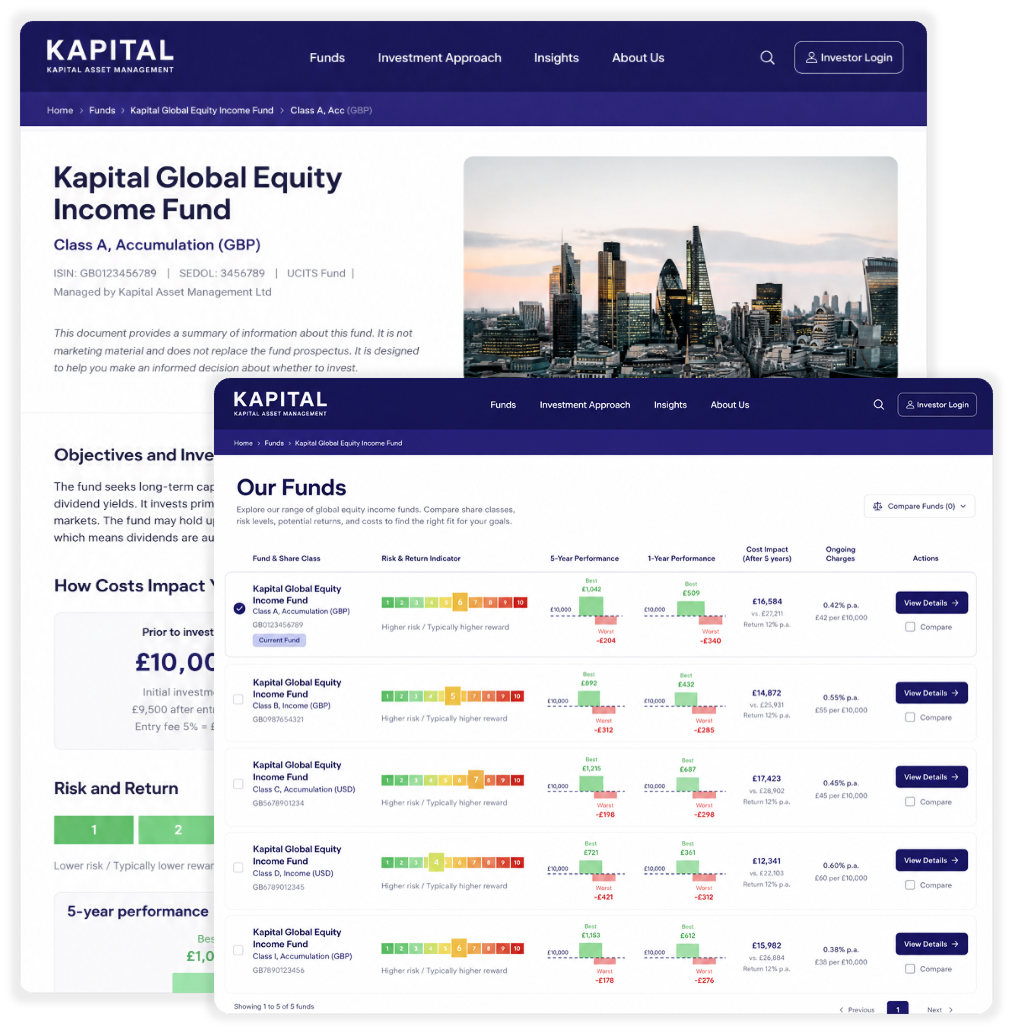

Every CCI manufacturer must produce a Product Summary for each in-scope product, updated at least annually. Design is flexible; the content – costs, risk score, past performance – must follow FCA-standardised methods.

02

Standardised risk and return score

Calculated from 10-year annualised standard deviation. For CCI, the risk and return score applies three distinct rules – pre-set floors for high-risk product types (including CFDs, derivatives, VCTs and EIS), a +1 adjustment for products with illiquidity or exit restrictions, and a mandatory score of 10 where investors can lose more than they invested

03

Information transparency

All information that affects the investor’s return – direct or indirect – must be described clearly, fairly and not misleadingly. A machine-readable Core Information file must be provided to all distributors.

04

Target market disclosure

Manufacturers must publish the product’s intended target market, risk profile and distribution strategy. Distributors must surface the Risk and Return Score and costs before any sale is completed.

05

Digital layering and public hosting

The FCA supports digital-first disclosures: most critical information first, detail accessible below. Both the Product Summary and machine-readable Core Information must be publicly hosted at all times.

06

The past performance line graph

A 10-year standardised line graph showing historical returns, displayed prominently with a mandatory “past performance is not a reliable indicator of future results” warning.

A PDF isn't enough. Here's what distributors actually need.

The FCA‘s CCI rules require more than a compliant PDF. Every Product Summary must be accompanied by a machine-readable Core Information file – typically a CSV or XML – that distributors use to ingest your data into their own platforms, portals, and sales journeys. Without it, your fund either doesn’t appear on distributor systems or appears with gaps.

Most CCI vendors give you a PDF generator. Kurtosys gives you both – the Product Summary and the structured data file, from the same pipeline, updated automatically whenever your data changes.

HOW KURTOSYS HELPS

From raw fund data to compliant disclosure - in four steps

Kurtosys handles the full CCI pipeline: configuring calculation parameters, running FCA-mandated metrics, generating Product Summary documents, and publishing them across your fund websites and distribution channels. All automated. All auditable.

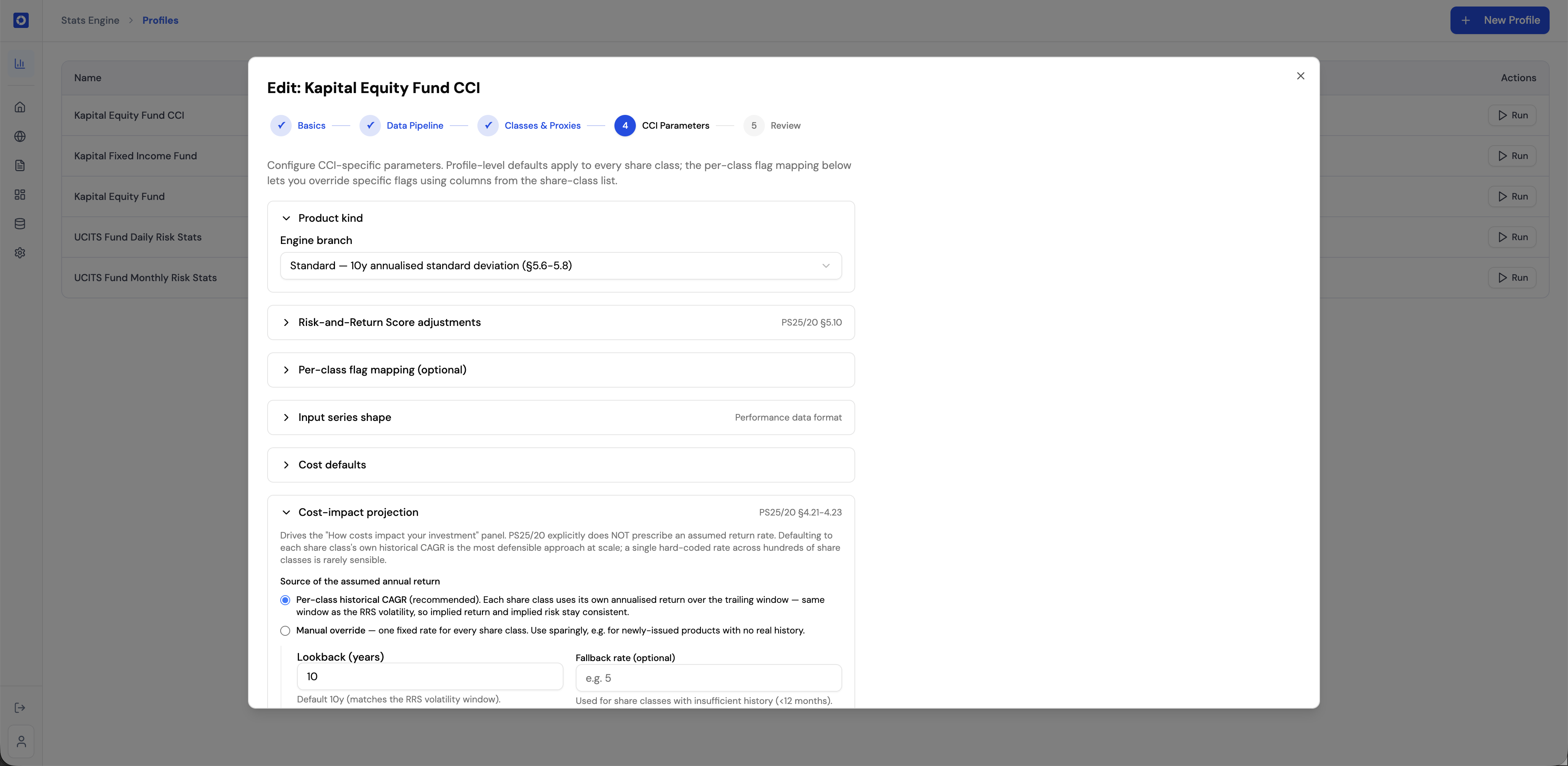

CCI calculation parameters set once, applied across every share class

The Kurtosys Stats Engine lets investment managers configure all CCI-specific parameters at profile level – product kind, risk engine branch (10-year annualised standard deviation per PS25/20), cost defaults, and cost-impact projection methodology.

- Standard and structured product engine branches supported

- Per-class historical CAGR or manual assumed return rate

- 10-year lookback window to match FCA calculation requirements

- All parameters referenced to PS25/20 sections for full audit traceability

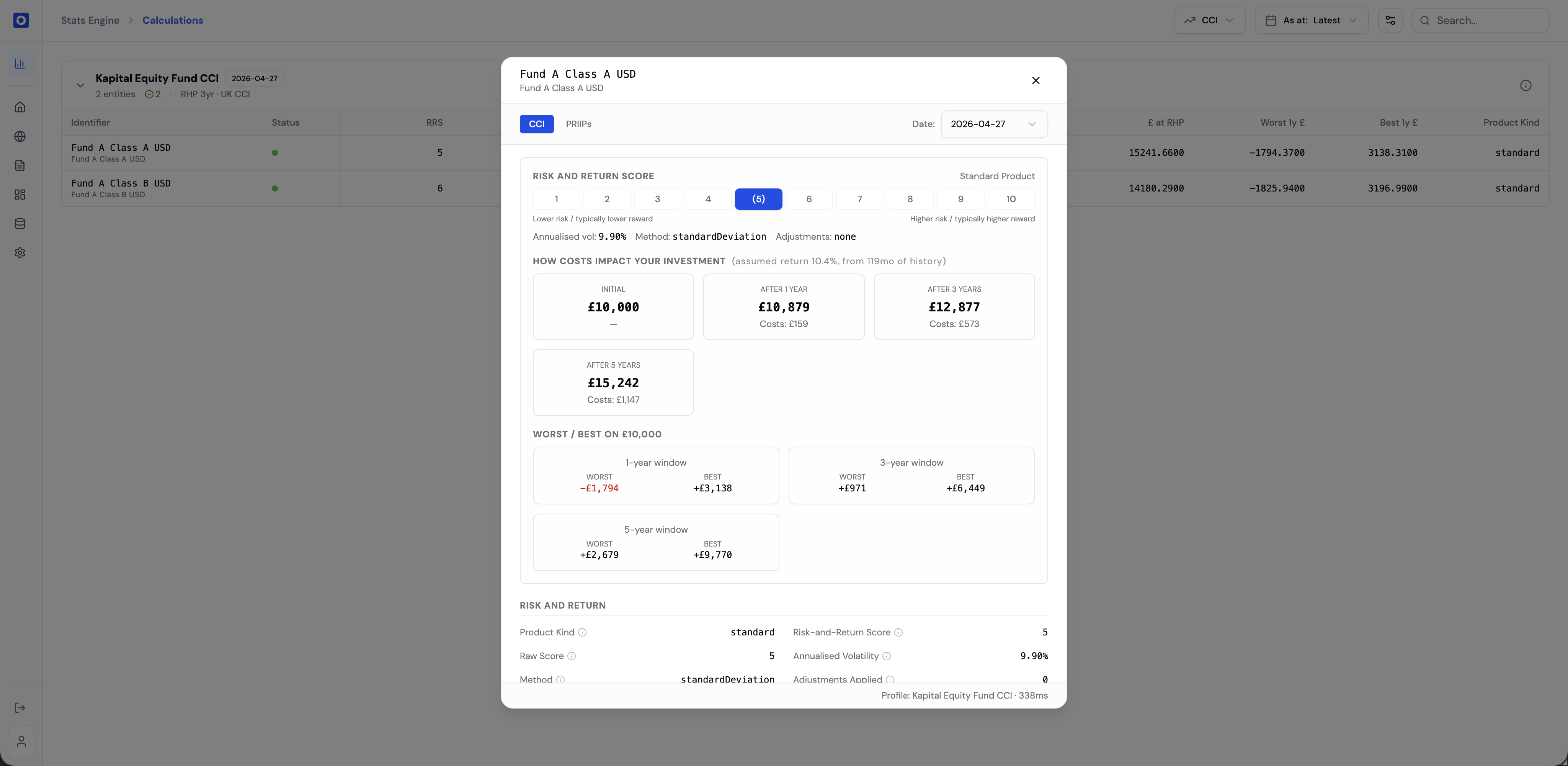

All FCA-mandated metrics calculated automatically from live fund data

The Stats Engine calculates every required CCI metric per share class: the Risk and Return Score and annualised volatility. Toggle between CCI and PRIIPs views where both regimes apply.

- Standard and structured product engine branches supported

- Per-class historical CAGR or manual assumed return rate

- 10-year lookback window to match FCA calculation requirements

- All parameters referenced to PS25/20 sections for full audit traceability

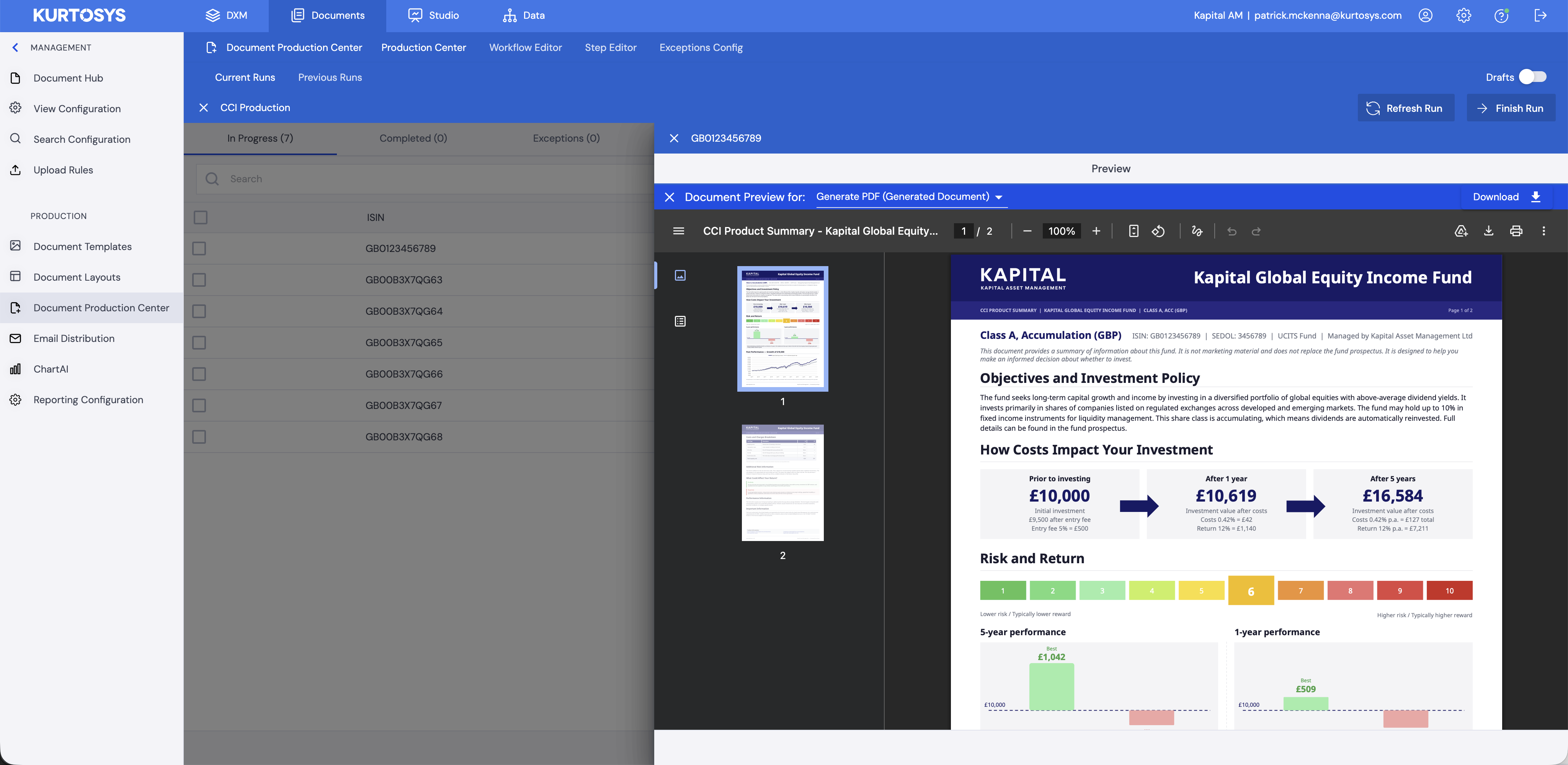

Compliant CCI Product Summaries produced without manual data entry

Kurtosys Studio for Office connects directly to live fund data and CCI calculations to build Product Summary documents in PDF and web-ready formats. Configure a template once and it scales automatically to thousands of share classes.

- Data-driven templates – zero manual data entry across your entire fund range

- CCI Product Summary in PDF and web-ready formats

- Costs breakdown, Risk and Return scale, and past performance charts included

- Multilingual output for cross-border distribution

Bulk production and distribution across every fund and channel

The Kurtosys Document Production Center runs CCI document production at scale across an entire fund range. Completed documents are automatically distributed to fund websites, document libraries, and distributor data feeds – meeting the FCA’s requirement that Product Summaries and Core Information are publicly accessible at all times.

- Bulk production across hundreds of ISINs in a single run

- Real-time progress tracking with exception flagging

- Previews and approvals workflow before publish

- Automated distribution to web, email and distributor data feeds

The five questions investment managers ask most about CCI

Authoritative answers written by jet. This reference covers the regulatory detail behind the regime - written to be useful whether or not you choose jet to solve it. Not legal advice.

What is the FCA CCI regime and how does it differ from PRIIPs?

The Consumer Composite Investments (CCI) regime is a UK-specific retail investment disclosure framework introduced under the Consumer Composite Investments (Designated Activities) Regulations 2024 and finalised by the FCA in Policy Statement PS25/20 in December 2025. It replaces both the PRIIPs Key Information Document (KID) and the UCITS Key Investor Information Document (KIID) with a single, flexible Product Summary Document that every manufacturer must provide to retail investors before purchase.

Rigid four-page KID template replaced by a flexible Product Summary. Firms control layout, length and medium.

Procedural under PRIIPs. Interpretative under CCI - investment managers must exercise judgement at every step.

PRIIPs scenario projections removed - replaced by standardised past performance and historical return windows.

PRIIPs was designed around paper. CCI is explicitly digital-first, supporting layered interactive disclosures.

What must a CCI Product Summary Document contain?

The FCA has not prescribed a fixed layout but has mandated specific content under PS25/20. The Product Summary must be technology neutral, outcomes focused, standardised only where needed, and structured so investors can access the right information at the right time.

Objectives and investment policy in plain language accessible to a retail investor with no specialist knowledge.

The standardised 1-to-10 score with a plain-English narrative explaining what it means for the investor.

All direct and indirect costs - ongoing charges, transaction costs, entry, exit, and performance fees.

Monetary effect of costs on a reference investment at one, three, and five years - shown in pounds.

Standardised historical data allowing comparison across products. Scenario projections no longer permitted.

Type of investor the product is designed for, including risk appetite and characteristics that make it unsuitable.

Minimum recommended investment horizon, clearly stated for investor liquidity assessment.

How investors can complain, including reference to the Financial Ombudsman Service where applicable.

A separate CSV file containing standardised cost and risk data for distributors to ingest and display.

How is the CCI Risk and Return Score calculated?

The CCI Risk and Return Score is a standardised metric on a scale of 1 (lowest risk) to 10 (highest risk) - broader than the PRIIPs Summary Risk Indicator, which used a 1-to-7 scale. The calculation method varies by product type.

10-year annualised standard deviation of weekly or monthly returns, per PS25/20 sections 5.6 to 5.8. Volatility mapped to 1-to-10 scale using FCA-defined breakpoints.

The raw score must be increased by at least one point to reflect the risk that investors may be unable to exit the product when they need to.

Value-at-Risk Equivalent Volatility (VEV) model converts the product's potential loss distribution into a volatility-equivalent figure on the same 1-to-10 scale.

In all cases, the score must be accompanied by a plain-English narrative in the Product Summary explaining what it means for the investor - not the number in isolation.

What are the key differences between CCI and PRIIPs for fund managers?

The six most operationally significant differences between the outgoing PRIIPs regime and the new CCI framework:

PRIIPs KID

Rigid four-page template prescribed by regulation.

CCI Product Summary

Fully flexible - firms control layout, length, language and format.

PRIIPs KID

Summary Risk Indicator: 1 to 7, combining market and credit risk.

CCI Product Summary

Risk and Return Score: 1 to 10, based on 10-year standard deviation.

PRIIPs KID

Mandatory scenario projections - widely criticised as misleading.

CCI Product Summary

Scenario projections removed. Replaced by standardised past performance data.

PRIIPs KID

Not mandated - distributor data sharing was market practice only.

CCI Product Summary

Mandatory - manufacturers must provide Core Information to every distributor.

PRIIPs KID

Designed around a paper document. Digital permitted but not designed for.

CCI Product Summary

Explicitly digital-first. FCA supports layered interactive disclosures.

PRIIPs KID

No requirement to monitor whether disclosures were read or understood.

CCI Product Summary

Embedded in Consumer Duty. Firms must evidence disclosures are being consumed.

What steps do investment managers need to take before 8 June 2027?

CCI is not simply a document update - it requires changes to data infrastructure, website architecture, distribution agreements, and monitoring processes.

Product summary document

Every CCI manufacturer must produce a Product Summary for each in-scope product, updated at least annually. Design is flexible; the content – costs, risk score, past performance – must follow FCA-standardised methods.

Standardised risk and return score

Calculated from 10-year annualised standard deviation. For CCI, the risk and return score applies three distinct rules - pre-set floors for high-risk product types (including CFDs, derivatives, VCTs and EIS), a +1 adjustment for products with illiquidity or exit restrictions, and a mandatory score of 10 where investors can lose more than they invested.

Information transparency

All information that affects the investor's return – direct or indirect – must be described clearly, fairly and not misleadingly. A machine-readable Core Information file must be provided to all distributors.

Target market disclosure

Manufacturers must publish the product's intended target market, risk profile and distribution strategy. Distributors must surface the Risk and Return Score and costs before any sale is completed.

Digital layering and public hosting

The FCA supports digital-first disclosures: most critical information first, detail accessible below. Both the Product Summary and machine-readable Core Information must be publicly hosted at all times.

The past performance line graph

A 10-year standardised line graph showing historical returns, displayed prominently with a mandatory "past performance is not a reliable indicator of future results" warning.

Ready to get ahead of the deadline?

See your CCI-compliant fund pages built live.

The Kurtosys team will walk investment managers through a hands-on demo – from data ingestion and CCI calculation to investor-facing fund pages – configured around your specific fund range and distribution channels.